Personal Banking | June 10, 2026

- Share:

Email

Email

Opening or closing a credit card might seem like a small move, but it can have a surprising impact on your credit score. While any changes are usually temporary, being intentional with your credit card habits can help protect your score — and even improve it.

Credit scores are made up of several different factors. That’s why opening or closing a card doesn’t automatically “hurt” your credit , but it can influence certain parts of your score.

What Makes Up Your Credit Score?

Your credit score is made up of several factors that help lenders understand how you manage debt and borrowing over time. Understanding these categories can help you make more informed decisions when opening or closing a credit card.

According to myFICO, here’s how your score is typically calculated:

- Payment History (35%)

- Amounts Owed / Credit Utilization (30%)

- Length of Credit History (15%)

- Credit Mix (10%)

- New Credit Inquiries (10%)

Each of these factors plays a role in your overall financial picture, which is why opening or closing a credit card can sometimes affect your score.

Want to understand why these factors matter? Check out why good credit is important to see how your credit score can affect your financial future.

Does Opening a New Credit Card Hurt Your Credit Score?

A small dip in your credit score after applying for a new credit card is common. For many people, the impact is temporary; especially when the card is used responsibly and payments stay on track.

One of the biggest mistakes after opening a new card is increasing spending too quickly. While it may be tempting to take advantage of a higher credit limit or rewards program, carrying larger balances can increase your credit utilization ratio, which may negatively affect your score.

Opening a new card can also make it easier to overspend without realizing it. Small purchases can add up quickly if balances aren’t paid down regularly.

To help maintain a healthy credit score after opening a new card:

- Keep balances as low as possible.

- Avoid making large unnecessary purchases right away.

- Pay at least the minimum payment on time each month.

- Try to pay the balance in full whenever possible.

- Use the card for planned purchases you have already budgeted for.

Using a credit card carefully over time can help build positive credit habits and strengthen your payment history.

Tip: Use your new personal credit card sparingly and pay off the balance in full each month to boost your credit score over time. This builds a positive payment history and keeps your utilization low.

Does Closing a Credit Card Hurt Your Credit Score?

Watch your credit utilization ratio: Your credit utilization ratio compares how much you owe to your total credit available. If you close a card, you reduce your available credit — which could cause your utilization to spike.

Let’s say you carry a $3,000 balance and have $10,000 in available credit (30% utilization). If you close a card with a $5,000 limit, your available credit drops to $5,000 — and your utilization jumps to 60%, which can negatively impact your score.

Even if your spending stays the same, closing a card can make your balances take up a larger percentage of your available credit.

When closing a card may make sense:

- You’re paying a high annual fee with no benefit.

- The card encourages overspending.

- You’re consolidating and simplifying accounts.

If You Decide to Keep the Card Open

If the card doesn’t cost you anything to keep, leaving it open may help maintain your available credit and length of credit history. To keep the account active:

- Use it occasionally (e.g., for a streaming subscription).

- Pay off the balance in full each time.

- Keep it open to maintain your available credit and length of credit history.

Before You Close a Credit Card

Before closing a credit card, it’s worth taking a few minutes to look at how the decision could affect your overall credit health.

- Is it your oldest account? Older credit accounts can help strengthen the length of your credit history, which is one factor used in calculating your score.

- Will your credit utilization increase? Closing a card lowers your total available credit. If you carry balances on other cards, your credit utilization ratio could increase, even if your spending stays the same.

- Does the card charge annual fees? If the card has a high annual fee and you’re no longer using the benefits, closing it may make financial sense.

- Do you have another active credit card? Having at least one active credit account can help maintain your credit history and show consistent credit usage over time.

- Are you simplifying your finances? Sometimes closing a card is about reducing stress, avoiding overspending, or managing fewer accounts. That can be a valid reason, especially if the card no longer fits your financial goals.

Taking time to review these factors can help you make a more informed decision before closing an account.

How to Maintain a Strong Credit Score

Your credit score is influenced by several factors, including how much credit you’re using and how long you’ve had credit. By being strategic when opening or closing credit cards, you can protect — or even improve — your credit score over time. The good news is that strong credit habits are usually built through small, consistent decisions. Paying balances on time, keeping utilization manageable, and avoiding unnecessary debt can all make a difference.

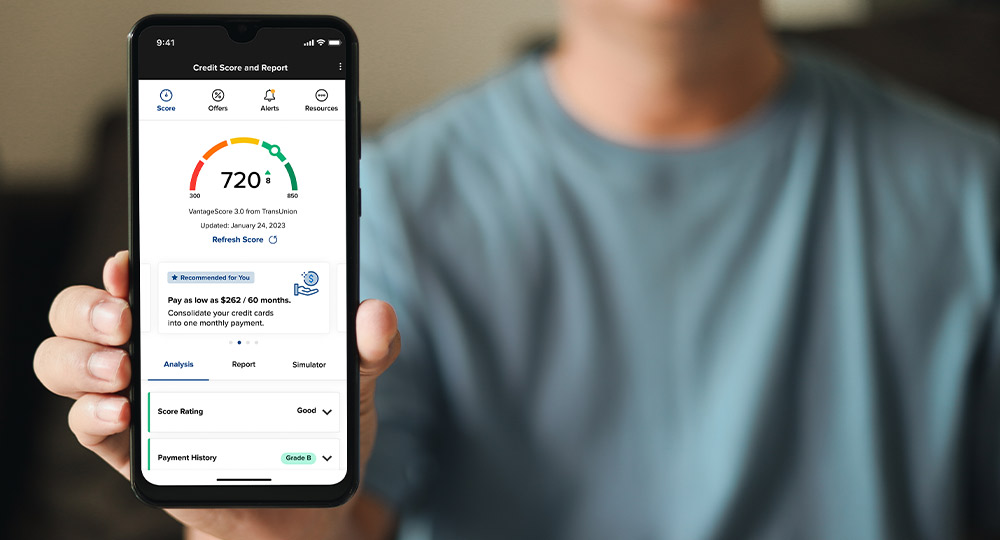

To stay on top of changes, consider using a tool like Credit Score Journey, available within digital banking at at Forward Bank. It helps you track your score, understand what’s affecting it, and gives you tips to keep moving forward financially.

Related Resources

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice. It may not be used for the purpose of avoiding any federal tax penalties. Please consult legal or tax professionals for specific information regarding your individual situation. The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.